4 min read

Offshore Energies UK's Decommissioning Insight 2025 report was published this week at the annual Offshore Decomissioning Conference in St Andrews.

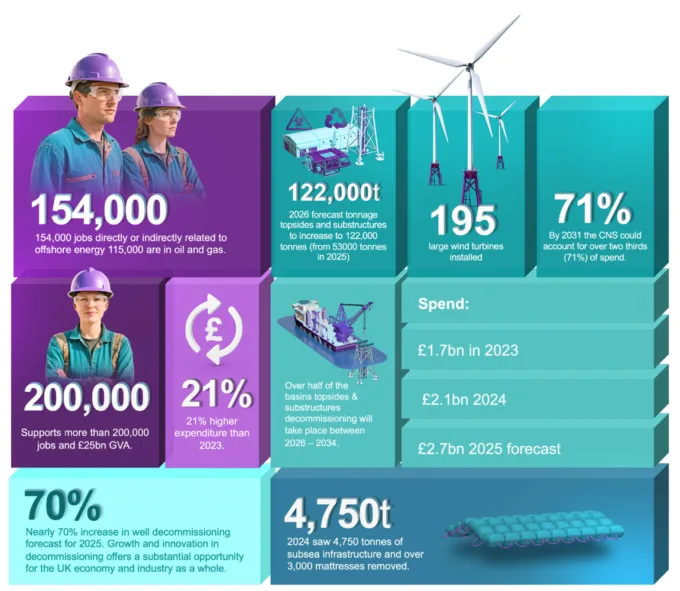

With £23 billion of activity forecast by 2035, a record £2 billion of annual spend expected this year, and more than 2,100 wells still to be decommissioned, the scale and opportunity ahead is crystal clear.

Across the two days there was a common theme. The world is watching how the UK delivers decommissioning in the North Sea. As John Gilley highlighted in his opening keynote, what happens here will set the tone for how basins around the world approach their own decommissioning programmes. But to lead, we cannot keep doing things the same way. We need the confidence and creativity to ask: what if we tried this instead?

That message sat alongside another from David Whitehouse. Decommissioning is no longer a footnote to the UK’s energy story. It is a central pillar of our industrial and economic future, and it must be delivered with pace, predictability and purpose.

Against that backdrop, I had the privilege of chairing a panel with five leaders who understand the landscape from every angle – legal, regulatory, operational, subsurface and energy transition:

- Valerie Allan, Partner, CMS Scotland

- Pauline Innes, Director of Decommissioning and Supply Chain, North Sea Transition Authority

- David Wilson, Decommissioning, Projects and Engineering Director, TAQA Group

- Teresa Munro, Chief Operations Officer, OPRED, Department for Energy Security and Net Zero

- Professor John Underhill , Interdisciplinary Director for Energy Transition and Professor in Geoscience and Energy Transition, University of Aberdeen

Here are my five takeaways from a packed conference full of engaging discussions on stage and in rooms and corridors surrounding the auditorium.

1. Decommissioning is underway and the legal framework is being tested

As Valerie Allan highlighted, decommissioning is no longer a theoretical exercise. It is already placing real pressure on contractual and regulatory frameworks that were never designed for the scale and complexity now unfolding.

Historic Joint Operating Agreements and contractual provisions were written for a different era. Operators are now having to interpret clauses that were intentionally light touch, while also dealing with the uncertainty of ageing assets and inconsistent subsurface data. This makes risk allocation, estimating, pricing and contracting materially harder.

Her point was clear. Decommissioning sits within a much wider commercial and regulatory ecosystem. The frameworks that support it now need to adapt at the same pace as the activity itself.

2. Regulatory pace must improve, but legal robustness remains essential

Both Pauline Innes and Teresa Munro were frank about the pressure on the regulatory system. OPRED and the NSTA have taken steps to simplify approvals, clarify expectations and streamline processes, but operators are still experiencing delays that impact planning, contracting and commercial certainty.

At the same time, they were equally clear that approvals cannot and will not be rushed. Every programme and every asset is different, and decisions must remain legally sound and defensible. That is non-negotiable.

The direction of travel is encouraging. Simplified guidance is being reviewed, cross-regulator collaboration has strengthened and stewardship tools are improving. The priority now is aligning increased pace with unchanged legal rigour.

3. The supply chain is world-leading, but it needs certainty to invest

David Wilson described a supply chain that is both highly capable and increasingly constrained. More than 70 per cent of TAQA’s decommissioning spend remains within the UK, and the quality of work being delivered across subsea, heavy lift and specialist services is impressive.

Yet the challenges are becoming more acute. Vessel availability is tightening. Inflation and complexity are rising. Workforce capability is strong, but institutional knowledge is not always shared across the basin. And the stop–start nature of the pipeline is preventing companies from investing at the scale required.

This is where John Gilley’s themes resonate so strongly. The supply chain needs continuity. It needs predictable sequencing. It needs visibility of what is coming and when. Without that, companies cannot plan, invest or scale the capability that decommissioning at pace requires.

4. The offshore system must be managed as an integrated whole

Professor John Underhill underscored a point that goes beyond decommissioning. The offshore environment is becoming increasingly crowded, with oil and gas, wind, CCS, cables, pipelines and decom all competing for space and priority. Decisions made in one part of the system can significantly constrain or enable another.

His reflections fell into three areas.

First, access to legacy wells is fundamental for future carbon storage. If a well is later identified as a potential leakage pathway, operators will need access regardless of who holds adjacent licences.

Second, P&A data must be released consistently to support CCS site selection, safety assessments and long-term planning. And third, government and regulators will need to take a more strategic view of offshore spatial planning to avoid conflicts and ensure future-proofing across all offshore energies.

The subsurface does matter, but so does the integrated management of the entire offshore energy system.

5. Confidence, clarity and collaboration will determine UK's leadership

If one theme dominated the conference, it was this. Decommissioning is a once-in-a-generation industrial programme that the UK can lead globally – but only if the system becomes more predictable, more integrated and more confident.

Confidence comes from stable regulatory processes, credible timelines and clear pathways to approval. Clarity comes from consistent expectations, transparent data requirements and better sequencing of activity. And collaboration comes from early, sustained engagement across operators, regulators, the supply chain and academia.

This is what will enable the shift John Gilley described. A shift from doing what we have always done to exploring alternative approaches, challenging accepted norms and setting an international benchmark for what responsible, efficient and future-focused decommissioning can look like.

OEUK Offshore Decommissioning Report 2025

The road ahead

The next decade will define the UK’s decommissioning industry. The sale is unprecedented, the complexity is rising and the stakes are high. But the capability exists, the ambition is real and the opportunity is significant.

Thank you to OEUK for creating a platform for such a wide-ranging and open discussion and congratulations to Ricky Thomson - CEng FIMechE CMgr FCMI and his team. Thank you to the five expert panellists for their depth of insight. And thank you to the audience of more than 400 industry professionals for their questions, candour and contributions.

If the UK gets this right, the North Sea will not just be decommissioned. It will become the global exemplar for how mature basins can manage their past while enabling the integrated, low-carbon energy systems of the future.