4 min read

When America sneezes, the climate often catches cold. Donald Trump’s move to reverse the Obama-era “endangerment finding” – the legal foundation for federal controls on greenhouse gases – looks like a technical fight. It is not. It is a reminder that climate policy in the world’s largest economy can still be dismantled by politics, not science.

For UK energy companies, the immediate impact is indirect. But the signal is clear. The global regulatory environment is becoming more volatile. Less predictable. More contested. Boards are being asked to invest over 20-year horizons while governments struggle to plan beyond the next election. In that environment, regulatory uncertainty becomes a cost in its own right. It raises the price of capital. It delays final investment decisions. It makes long-term infrastructure harder to finance.

And it creates a new central question for energy firms: which direction will global regulation ultimately take?

Britain’s problem is not ambition. It is clarity.

On paper, the UK’s position looks stable. Net Zero by 2050 is law. Carbon budgets provide structure. Offshore wind is supported through Contracts for Difference (CfDs). The UK Emissions Trading Scheme provides an increasingly meaningful carbon price.

Yet targets do not equal certainty. Companies can work with almost any policy, provided it is consistent. What they struggle with is improvisation: sudden tax changes, shifting auction rules, mixed political messaging, and unclear signals about the role of oil and gas, hydrogen, carbon capture and storage (CCS), and long-duration power storage.

This is not a theoretical concern. It is now the central investment issue.

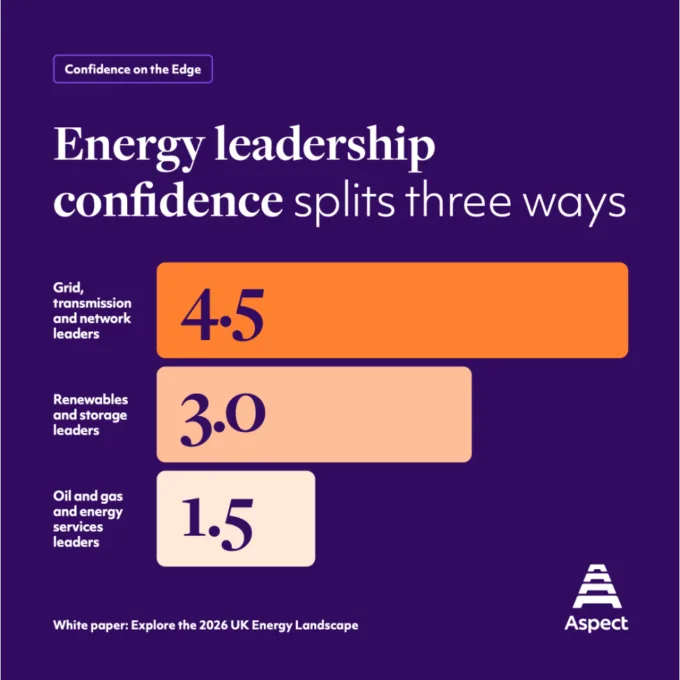

Aspect’s recent white paper Confidence on the Edge captures the mood across the UK energy system: broad alignment on the direction of travel, but weaker confidence in delivery and policy credibility. It makes the point bluntly: “capital will not flow” if leaders do not believe the future is worth betting on.

In other words, uncertainty is not just a communications challenge. It is a drag on delivery.

Aspect White Paper: Confidence on the Edge

The regulatory battle is global – and investors are watching

The bigger issue is that UK policy does not sit in isolation. Capital is mobile. So are supply chains. And energy companies operate across jurisdictions. The real question is not whether Britain will stay broadly committed. It is whether the global balance of regulatory power will tilt towards rollback or acceleration.

America, under Trump, is signalling rollback. Not only of specific rules, but of the principle that climate policy is durable. That matters because the US has historically shaped global standards, corporate behaviour and investor expectations. If federal policy becomes openly reversible, the world’s largest pools of capital will begin to treat decarbonisation policy as political risk rather than industrial strategy.

Europe is pushing in the opposite direction. The EU continues to tighten emissions regulation, strengthen reporting requirements, and use trade tools to reinforce decarbonisation through mechanisms such as carbon border measures. Brussels is not treating climate policy as optional. It is treating it as market design.

China remains strategically ambiguous. It continues to build coal capacity while dominating clean-tech manufacturing and export supply chains. But the direction of travel is clear: it intends to own the industries of the future, regardless of its near-term emissions curve.

The Gulf states are hedging. They are investing in hydrogen, renewables and industrial diversification, while defending oil and gas as long as global demand persists. Their approach is not ideological. It is pragmatic.

This is the landscape UK firms must navigate: a world where regulation is no longer converging but competing.

Who prevails?

The temptation is to assume that America’s reversal will slow everything. That is possible. But the more likely outcome is fragmentation rather than reversal.

The EU’s approach will continue to shape global corporate behaviour, because access to European markets requires compliance. China will shape it because it controls supply chains. The Gulf will shape it because it controls low-cost hydrocarbons and increasingly deployable capital. Even if Washington retreats, these forces do not disappear.

The question for energy companies is therefore not whether the transition survives, but what kind of transition survives: one led by rules, trade policy and standards (the EU model), or one shaped by domestic political cycles and deregulation (the US risk).

For now, Europe’s regulatory architecture looks more durable. America’s looks more exposed. That means the likely long-term direction remains towards tighter requirements, not looser ones – even if the journey becomes messier and slower.

The UK’s priority is to reduce ambiguity

The UK cannot control Washington. But it can control its own credibility.

If the UK wants to remain investable, it needs greater operational certainty. Clearer planning reform. Clearer auction schedules. Clearer long-term fiscal and regulatory signals.

The energy industry is not asking for special treatment. It is asking for stability.

In that sense, Trump’s move is a warning shot. Not because it changes the physics of decarbonisation, but because it reminds investors how quickly the politics can turn. Countries that provide clarity will win capital. Those that offer volatility will pay a premium.

What companies should do now

- Plan for diverging global regulation, not a single aligned pathway

- Build political risk into investment cases, not as an afterthought

- Push government for clarity and sequencing, not just new targets

- Strengthen investor confidence through credible disclosure and delivery milestones

- Communicate consistently and plainly, especially on costs, trade-offs and timelines

- Treat trust as strategic infrastructure - without it planning and delivery will fail